If you’ve ever been surprised by the cost of a blood panel your doctor ordered, or watched a pharmacy charge you $80 for a generic medication your insurance “covered,” you already understand the problem. The traditional healthcare pricing model isn’t built for transparency. It’s built for intermediaries.

Direct Primary Care strips that out. And at Long Life Med, the savings on labs and medications alone can offset a significant chunk of your membership cost.

How Lab Savings Work Under DPC

In the insurance-based system, labs go through a chain: your doctor orders them, a third-party lab processes them, the lab bills your insurance, your insurance negotiates a rate, and whatever’s left hits your deductible or co-pay. You rarely know the price in advance. And if you haven’t met your deductible, you’re paying retail rates that are often wildly inflated.

DPC clinics like Long Life Med bypass that chain. Because the clinic orders labs directly at wholesale pricing, members pay a fraction of what they’d pay through insurance or at a retail lab. Your provider discusses costs upfront before anything is ordered. No surprises. No explanation of benefits arriving weeks later, with a number you didn’t expect.

Every DPC membership tier at Long Life Med includes labs as part of the plan:

Standard ($100/month or $1,000/year): Annual labs included. If you prepay annually, you unlock a $125 lab credit plus up to 10% off additional services and products.

Preferred ($200/month or $2,000/year): Semi-annual labs included, with extras like advanced cardiac panels (apolipoprotein evaluation).

Annual prepay unlocks a $400 lab credit, a $100 supplement credit, and up to 20% off additional services.

Executive ($500/month or $5,000/year): Quarterly labs included, with advanced cardiac panels and genetic testing. Annual prepay unlocks a $1,500 lab credit, a $500 supplement credit, and up to 30% off additional services.

Those lab credits apply toward any additional testing your provider recommends beyond what’s already included. For a patient doing a functional medicine workup that involves hormone panels, inflammatory markers, nutrient levels, and gut health assessments, those credits add up fast.

How Medication Savings Work

DPC clinics operate outside the insurance formulary system. That means your provider isn’t constrained by what an insurance company has decided to cover or which manufacturer cut them the best deal. They can prescribe what’s clinically appropriate and help you source it at the lowest available price.

Long Life Med offers wholesale pricing on medications. The clinic can often source generics and certain compounded medications at prices well below what you’d pay at a retail pharmacy, even with insurance. For patients on ongoing prescriptions, particularly for hormone replacement, weight management medications, or chronic condition management, the difference between retail pharmacy pricing and wholesale DPC pricing can be substantial over the course of a year.

The stackable discounts increase savings further. Preferred members get up to 20% off, and Executive members get up to 30% off, on supplements and other eligible products available through the clinic. Medications are already offered at wholesale pricing for all patients.

The Insurance Pricing Problem, Explained Simply

Most patients don’t realize this: having insurance doesn’t mean you’re getting a good price. It means you’re getting the price your insurance company negotiated, which isn’t always lower than what a DPC clinic can offer through direct wholesale relationships.

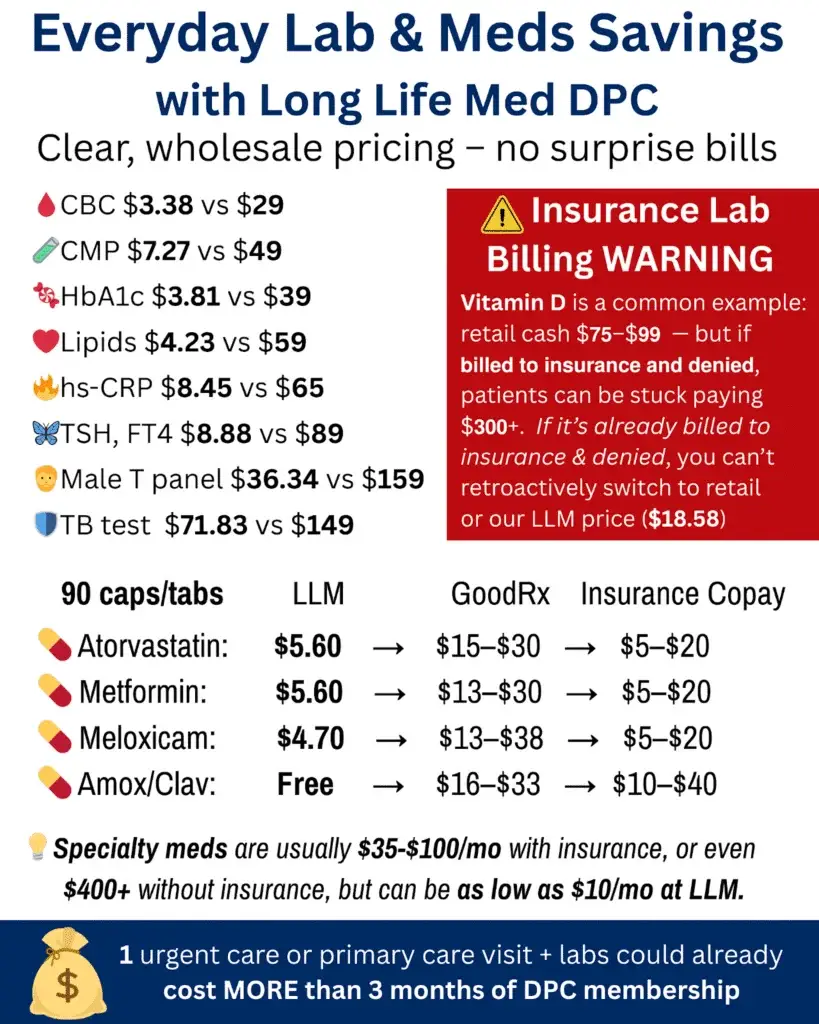

Lab work is a clear example. A comprehensive metabolic panel at a hospital outpatient lab might be billed at $200-$400 to your insurance. After “negotiation,” your cost might be $80-$150 against your deductible. Through a DPC clinic with wholesale lab pricing, the same panel might cost $15-$30. The difference is the middleman.

Medications follow a similar pattern. Insurance formularies push patients toward specific drugs based on rebate agreements, not clinical superiority. A DPC provider has no formulary to follow. They prescribe based on what works for you and help you find the most cost-effective way to fill it.

What This Means in Real Dollars

Consider a patient who needs quarterly lab work (hormone panels, metabolic markers, and inflammatory markers) and is on two ongoing prescriptions. In the insurance system, assuming a high-deductible plan:

Four rounds of labs at $150-$300 each: $600 to $1,200 per year. Two monthly prescriptions at retail pricing: $50-$150/month each, or $1,200 to $3,600/year. Total: roughly $1,800 to $4,800 annually, and that’s before office visit co-pays.

Under the Preferred DPC plan at $2,000/year: semi-annual labs are included, additional labs come at wholesale pricing with a $400 credit, medications are available at wholesale rates with up to 20% off, and every office visit, every urgent care visit, and every televisit is already covered. The total cost is more predictable, almost always lower, and you’re getting significantly more care.

The Executive plan at $5,000/year is designed for patients with more complex needs. With quarterly labs included, $1,500 in lab credits, $500 in supplement credits, and 30% off, it’s structured for patients doing intensive longevity, hormonal, or functional medicine protocols where testing and supplementation are frequent.

HSA and FSA Eligibility

All DPC memberships at Long Life Med are reimbursable through HSA (Health Savings Account) and FSA (Flexible Spending Account) with pre-tax dollars. That means you’re effectively getting a tax discount on top of the wholesale pricing. Related expenses like imaging, labs, and prescriptions are also HSA/FSA eligible.

For patients pairing DPC with a high-deductible catastrophic health plan, the HSA becomes particularly powerful: you fund it with pre-tax dollars, use it to cover your DPC membership and related care, and reserve the catastrophic plan for the rare, high-cost events that fall outside the clinic’s scope.

What Transparent Pricing Actually Looks Like

The $100 registration fee is waived for memberships prepaid for at least 3 months. Your provider discusses costs before ordering anything. You know what your membership covers. You know what falls outside it. And when something does fall outside your plan, you’re still getting wholesale pricing rather than retail.

That’s not a special perk. That’s what healthcare pricing should look like.

If you’re spending more than you should on labs, medications, or basic care in the Henderson or Las Vegas area, schedule a free first visit or call (702) 359-4510 to see how the numbers compare.